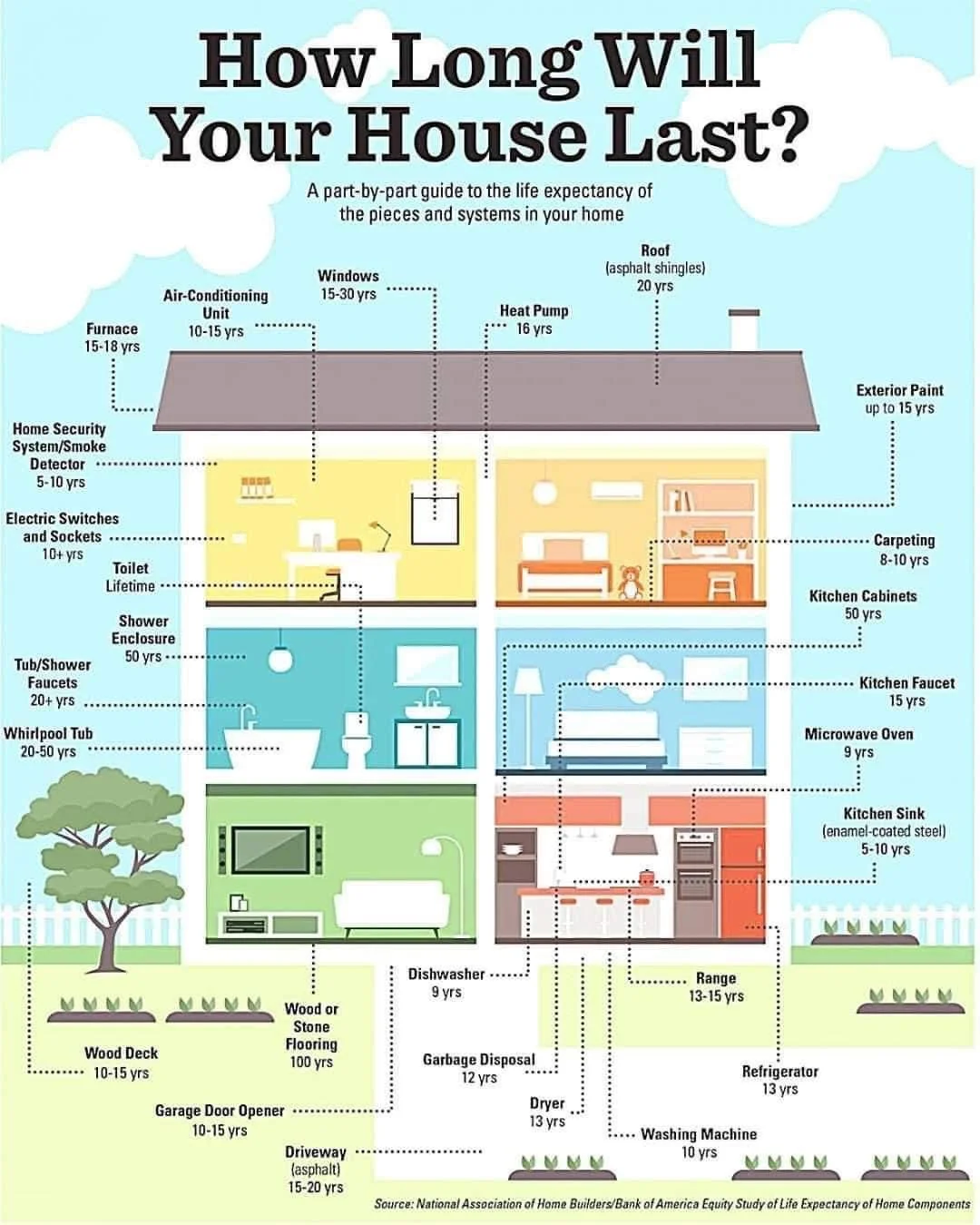

A Quick Guide on the Lifespan of Household Systems and Items

Understanding the expected lifespan of the various systems and items in your home is crucial for effective budgeting, maintenance planning, and overall household management. Knowing how long different components are likely to last can help you make informed decisions about repairs, replacements, and upgrades.

By being aware of the average lifespan of household systems and items, you can take proactive steps to maintain, repair, or replace them as needed. Regular maintenance and prompt attention to issues can help you maximize the longevity of your home's components, ensuring a comfortable and efficient living environment for years to come.

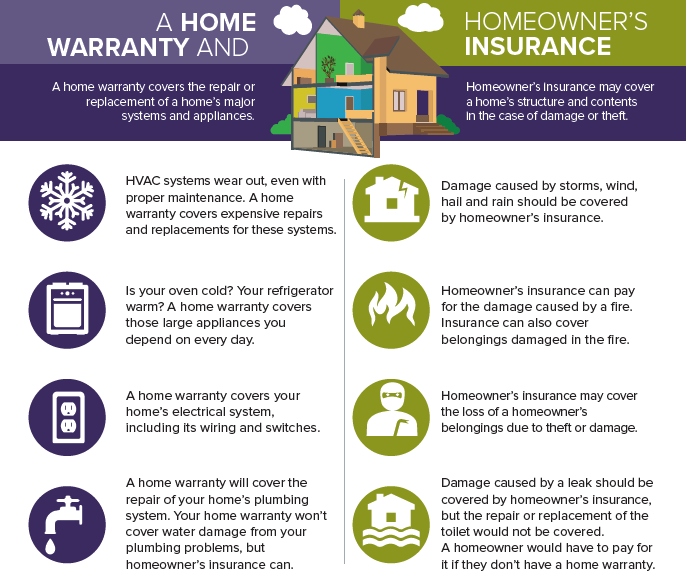

Know the Difference Between a Home Warranty and Homeowner’s Insurance

Knowing the differences between a home warranty and homeowner’s insurance can be a little confusing. But it’s important to understand where one begins and the other ends to make sure you have the coverage you need. Following is how to know the difference between a home warranty and homeowner’s insurance:

In a nutshell, a home warranty covers the repair or replacement of a home’s major systems and appliances. Homeowner’s insurance, on the other hand, may cover a home’s structure and contents in the case of damage or theft.

A HOME WARRANTY TYPICALLY COVERS THE FOLLOWING:

HVAC – Even with proper maintenance, an HVAC system can wear out. A home warranty covers expensive repairs and replacements for these systems.

APPLIANCES – Is your oven cold? Your refrigerator warm? A home warranty covers those large appliances you depend on every day.

ELECTRICAL SYSTEMS – A home warranty covers your home’s electrical system, including its wiring and switches.

PLUMBING SYSTEM – A home warranty will cover the repair of your home’s plumbing system. (Your home warranty won’t cover water damage from your plumbing problems but homeowner’s insurance can.)

HOMEOWNER’S INSURANCE TYPICALLY COVERS THE FOLLOWING:

WEATHER-RELATED DAMAGE – Damage caused by storms, wind, hail and rain should be covered by homeowner’s insurance. (Typically, damage caused by flooding isn’t covered unless there is flood damage insurance included.)

FIRE-RELATED DAMAGE – Homeowner’s insurance can pay for the damage caused by a fire, and also cover the belongings damaged in the fire.

BELONGINGS – Homeowner’s insurance may cover the loss of a homeowner’s belongings due to theft or damage.

LEAKS – Damage caused by a leak should be covered by homeowner’s insurance, but the repair or replacement of the toilet would not be covered. In this case, a homeowner would have to pay for it if they don’t have a home warranty.

The bottom line is that comprehensive home coverage includes both homeowner’s insurance and a home warranty.

Pre-listing tips to avoid inspection limitations this winter

It’s hard to believe, but the first frost is approaching and the cooling temperatures mean that inspections will be somewhat limited due to seasonal factors. Specifically these 3 common cold weather limitations:

A/C units cannot be operated in temperatures below 65 degrees F. This is an industry standard limitation that prevents risking damage to the components due to the viscosity of the oil in the compressor.

Snow covered roofs and exterior surfaces cannot be visually inspected (self explanatory)

Landscape irrigation systems and exterior hose bibs are winterized and cannot be tested. Inspection of the landscape irrigation systems is beyond the scope of a home inspection, but confirmation of these systems operating is often something that a buyer wants to check and cannot in the winter.

If you know that you will list your home for sale between now and late spring, here are some tips to help you prepare for a smooth inspection process.

Have the A/C unit professionally serviced by an HVAC technician with a written report confirming operation on that date. Make sure to schedule this prior to sub 65 degree days if possible as HVAC technicians are also limited by the temperature restriction.

Have the roof pre-inspected by a reputable roofing contractor with a photo report generated showing the condition of the roof on that date. Unless there are major storms between that inspection date and the buyer's inspection date, the chances of unforeseen damages are low.

Confirm operation of the landscape irrigation system before it’s winterized. This is something that your seller can even do on their own with photo evidence.

How to determine if a roof has impact resistant (Class 4) shingles

Can you tell if the roof has “impact resistant class 4 shingles”? Our homeowners insurance wants to know..

This is a question that we get almost daily as home inspectors and it’s a frustrating question because there is no way to visually determine if a shingle is impact resistant/class 4 rated. The only way to determine a shingles impact rating is by the manufacturer's spec sheet. Some shingles do have labeling on the back side of the shingle, but of course we can’t see that without ripping up a shingle.

Tip: If a roof is newer or if you have the contractor's information who installed the shingles, then we recommend contacting the contractor to see if product specifications are still available for that job. Sometimes there are extra shingles lying around the property, but that is rare and not reliable. Most often the answer is just not available and certainly something that the inspector cannot determine through the normal scope of an inspection.

Other non asphalt shingle roofing materials such as concrete tile or metal roofs are inherently impact resistant and don’t need a rating to determine impact resistance.

Next time you are advising your clients on a homeowners insurance application, keep this information in mind and see if you can help them track down documentation from when the roof was installed.

How Often Should a Home Be Painted?

Depending on the quality of paint and craftsmanship, the exterior siding of a home should be painted every 6-10 years. Signs of a failing paint job are peeling paint, cracking of caulking, and/or fading of the paint.

TYPICAL EXTERIOR PAINTING COST ESTIMATE

You can expect to pay around $3-5 per square foot for a professional exterior paint job. The estimate is based on the total square footage of the home, not to be confused with the square footage of the home exterior surface.

Buyers should consider these three things when purchasing a home with solar

We often get questions about what to consider when purchasing a home with a solar electric system. Since we are not the solar experts, we asked Solar RNR, our trusted local solar detach and reset contractor to get their advice.

Is the solar leased or owned? If the solar is leased, the buyer will likely need to qualify for the additional costs of the solar lease payments in the mortgage calculations as the lease payments affect the buyer's debt-to-income ratio.

Is the solar functioning correctly and was it installed and maintained properly? Solar RNR always recommends that the buyer have the solar panels inspected by a qualified professional before purchasing the home to know for sure.

What exactly are you getting? When purchasing a home with solar it's good to know exactly what you are receiving, because solar is not cheap. How much electricity is solar producing? Is there battery storage included? How old is the system? Is it still under warranty? These are all questions a buyer should be asking when purchasing a home with solar. If the seller is unable to answer these questions, a company like Solar RNR would be happy to come out & take a look.

How Much Does Aluminum Wire Repair Cost?

Aluminum wire can be safely repaired without rewiring a house. A qualified electrician that specializes in aluminum wire repair can repair all of the circuits throughout a home to safely fuse or pigtail copper and aluminum connections. Do beware that purple wire nuts are no longer an acceptable connection and that “COPALUM” or “Alumiconn Connectors” are the two currently accepted repair methods aside from rewiring a home.

Average aluminum wire repair costs run about $65/electrical connection with an average 2,200 square foot home costing around $5,500-$7,500 to completely and thoroughly repair.

Source: The Aluminum Wire Repair Company

What Are The Different Types Of Defective Electrical Panels?

The two most notorious defective electrical panels are the Federal Pacific Electric (FPE) Stab-Loc panels manufactured from the 1950’s-1980’s and the Zinsco and later Sylvania Electrical panels largely used in the 1970’s. These 2 brands are considered safety hazards that should be replaced.

A lesser known, but equally problematic electrical panel was the Challenger brand electrical panel in the 1970’s and 80’s and has similar issues with overheating and faulty circuit breaker function. Challenger panels should be evaluated by a licensed electrician to determine if that model is problematic.

Did someone say rebates and tax credits?!

In some instances, rebates through the city of Denver combined with federal tax credits can help offset the cost of an electrical panel replacement by up to $2600. Check out our energy efficiency resource guide to learn about these incentives and more.

What is the cost to replace?

It’s important to note that the expected service life on an electrical panel is around 40 years, so any panel older than 40 years should be evaluated for replacement. The cost of a panel replacement is generally between $3k-7k.

How Long Does A Typical Garage Door Opener And Motor Last?

A typical garage door opener should last 15 years. It’s not uncommon for them to last longer, especially if properly maintained, but 15 years is a good guideline.

Keep in mind that proper maintenance, frequency of use, and quality of the opener are all factors that help determine longevity.

Costs vary, but the installed cost of a new garage door opener is generally between $400-$900.